Source Link: https://analyzingalpha.com/algorithmic-trading-history

Algorithmic trading, also known as algo trading or black-box trading, is a form of artificial intelligence that automates trade. Algorithmic trading captures more than 50% of the trading volume in the US.

Here are some fascinating timelines of how algo trading evolved and gained prominence in recent years.

17th Century: Earliest Form of Information Arbitrage

In the early 1800s, Nathan Mayer Rothschild and his family used carrier pigeons to arbitrage prices of the same security by relaying the information before the computers did it.

Using the pigeon carriers, Rothschild was the first person to know about England defeating France at Waterloo. He also received market insights about Paris, Naples, Frankfurt, and Vienna through the pigeon carriers.

1832: Samuel Morse’s “The Telegraph”

Samuel Morse developed “The Telegraph” in 1832. It was a pathbreaking invention in the history of long-distance communications. It works by transmitting electrical signals through the connecting wire between stations.

He also developed a code, the Morse code. It involved dots and dashes used to transmit complex messages across telegraph lines.

In the trading industry, the Telegraph helped to distribute Financial newsletters in areas far away from the marketplace.

Later, by 1856, it also facilitated broker-assisted trading of exchange-based securities.

1850: Reuters News Transmission Services

In April 1850, Julius Reuter, the founder of Thomson Reuters, had an agreement with Heinrich Geller. They launched news transmission services between Aachen and Belgium using carrier pigeons. Its main purpose is to relay stock price information.

In October 1851, Julius Reuter established a telegraph office. It aimed to relay stock market quotations between London and Paris using the Calais-Dover telegraph cable under the English Channel.

In 1858, he convinced London Times and other English dailies to subscribe to his new service, which he named Reuters.

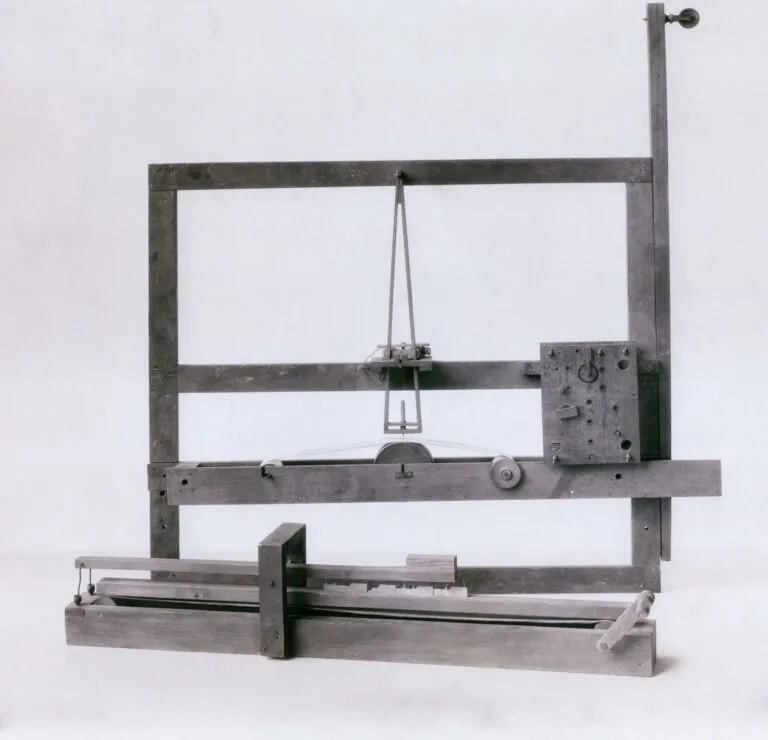

1867: First Stock Ticker

In 1867, Edward A. Calahan, an engineer at the American Telegraph Company, upgraded a telegraph machine for printing financial data for the stock market. This development saw a lot of success, and the word spread like lightning.

It allowed stockbrokers and traders to access recent stock price information without any physical presence at a stock exchange. This invention allowed the NYSE to centralize the order flow and improve liquidity.

Later, Calahan received orders for more batches, which were eventually known as stock tickers, as their printing wheels made ticking sounds like clocks.

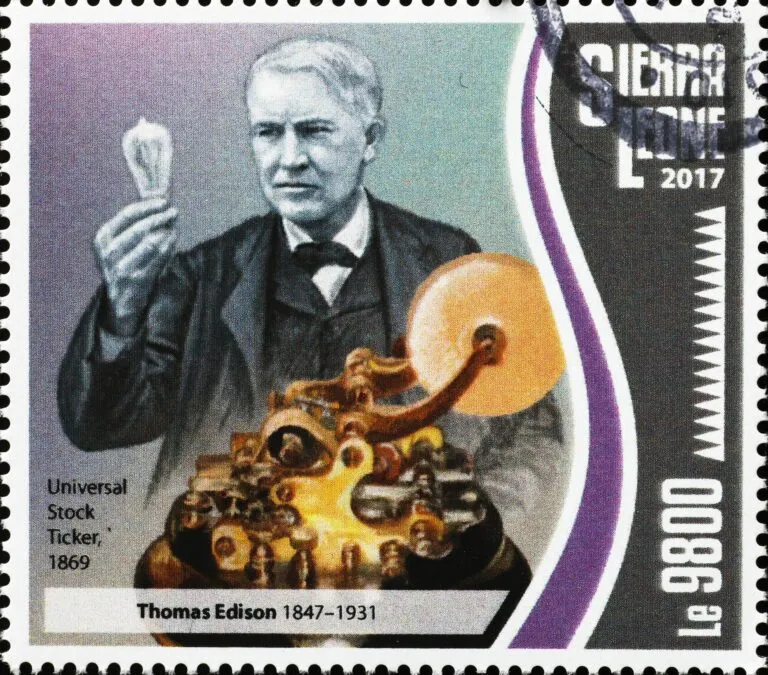

1871: Improved Stock Ticker

In 1871, Calahan’s stock ticker was improved by Thomas Alva Edison. He designed a new stock ticker called the Edison Universal Stock Printer. It was a Brass mechanism with a cast-iron base and glass dome with a blank roll of ticker paper and a base that said: “Quotations furnished by the Western Union Telegraph Co / Apply to the local manager.”

The developed ticker was the first mechanical mode for transmitting real-time stock market data directly from exchange floors to intermediaries and investors throughout the country.

1929: The ‘Big Board’ Was Installed

The Teleregister Corporation installed the first stock information display board in 1929. This “Big Board” was a large vertical electronic display located in an exchange. It laid the foundation of the “open outcry” trading system. In this system, traders met in a common location and made transactions based on the Big Board’s standard price and volume information vision.

1930: Western Union Launches 5-A

Western Union launched its Ticker-5A, a 500-character-per-minute “black box” processing up to 8 million trades a day.

1949: The First Trading Rule-Based Fund

An American trader, Richard Davoud Donchian, launched Futures, Inc in 1949. It is a publicly-held commodity fund trading the futures markets. It is the first to use predetermined rules to generate actual trading buy and sell signals. It is the earliest form of the automated trading system.

1952: The Markowitz Model

An American economist and the father of quantitative analysis, Harry Max Markowitz, introduced computational finance in the 1950s. It was meant to address the issue of portfolio selection. He developed the Modern Portfolio Theory or MPT for academicians in his article, “Portfolio Selection.”

Through his theories, Markowitz established the correlations between securities and diversification. He also emphasized the criticality of portfolios and risk.

1960: The First Arbitrage Trade Using Computers

Ed Thorp, Michael Goodkin, and Harry Markowitz became the first traders to employ computers for arbitrage trading in 1960.

1960: Quotron I and Ultronics

The Quotron I was developed by Jack Scantlin of Scantlin Electronics, Inc. It featured a magnetic tape desktop storage unit with a keyboard and printer. The data was recorded into the storage unit from the ticker line.

Robert S. Sinn also introduced Ultronics. These units were designed to monitor the last sale, bid, ask, high, low, total volume, open, close, earnings, and dividends for every stock, as well as the commodities market data.

1965: NYSE’s MDS I and MDS-II

Market Data System I (MDS I) was introduced to provide automated quotes. This program could provide over 100,000 trades a day and had seen a downtime of fewer than 21 minutes per year. The improved version of the system was then developed after several years and called MDS-II.

1967: Instinet Trading System

The Instinet Trading System is s the oldest electronic communications network on Wall Street. Instinet allowed large institutional investors to trade pink sheet or over-the-counter securities directly with one another in an electronic set-up.

This system has become a powerful competitor to traditional exchanges. It also provides advanced trading technologies such as the Newport EMS, trade cost analytics, and more.

1971: The Formation Of Nasdaq

In 1971, the National Association of Securities Dealers Automated Quotations (NASDAQ) was formed. It offered quotation and electronic trading. It is the second oldest stock exchange in the United States and the first to offer online trading.

1978: Intermarket Trading System

The Intermarket Trading System (ITS) is an electronic network that links the trading floors of various exchanges and allows real-time communication and trading between them.

1981: Bloomberg

In 1981, the Bloomberg terminal computer was developed. It contained financial data about stocks, bonds, and other investments. This development became a path-breaking innovation in the field of real-time information many years ago.

1982: Renaissance Technologies

Renaissance Technologies, a quant fund, was founded in 1982 by Jim Simons. These technologies helped predict price fluctuations of financial instruments by analyzing maximum data and looking for non-random price changes to make trading decisions.

1984: Dataspeed Launched Quotrek

In 1984, a wireless mobile stock quotation delivery system called QuoTrek was launched. This development was not successful because brokers already had access to the information that QuoTrek provided.

1984: NYSE Computerized Order Flow

The Computerized Order Flow began in the financial markets in the early 1970s. It significantly changed the trade execution interns of volume and speed. During this time, the process allowed orders up to 2,000 shares that could be electronically routed to a specialist.

1993: Interactive Brokers was Founded

In 1993, Thomas Peterffy, a pioneer in digital trading, founded Interactive Brokers. Its objective was to popularize the technology (the first handheld computer for trading) that Timber Hill developed for electronic network and trade execution services to customers.

1996: Island-an ECN

In 1996, an electronic communication network (ECN) known as “Island” was launched. It was a service where traders could receive information on stocks through an electronic feed once they subscribed to their services.

1998: Alternative Trading Systems-Reg ATS

US Securities and Exchange Commission (SEC) allowed electronic exchanges and paved the way for computerized High-Frequency Trading in 1998. Because of this, there was significant growth in high-frequency trading. In 2009, it had captured 70% of the US securities markets.

2001: US Decimalization Process Completion

US Decimalization is a process where security prices are quoted using a decimal format rather than fractions. With the Decimalization, there was a minimum tick size change, from 1/16 of a dollar (US$0.0625) to US$0.01 per share. This process, implemented in 2001, has encouraged algorithmic trading immensely.

2005: Regulation National Market System

The Regulation National Market System (reg NMS) was formulated in 2005 and established in 2007. It was a series of initiatives to modernize and strengthen the national market system for equities.

2008: The Creation of Pandas

The Pandas, mainly used for data analysis, was created in 2008 at AQR Capital Management. It is a data manipulation and analysis software package for the Python computer language. It supports data input from various file formats, including csv, JSON, SQL, and Microsoft Excel.

2010: Fastest Dark Fiber Services

Spread Networks launched the fastest dark fiber services in 2010. At 825 fiber miles and 13.3 milliseconds, it was the shortest between Chicago and New York.

2010: The Flash Card

The first flash card was in 2010. Flash Crashes are a semi-regular occurrence, sometimes impacting just a single stock or a broader market.

2011: Microchip by Nanotechnology

In 2011, Fixnetix, a London-based trading technology company, developed a microchip that had the power to execute trades in nanoseconds.

The microchip was called iX-eCute. It was a microchip for ultra-low latency trading, which included algorithmic trading systems and network routes. Financial institutions used these while connecting to stock exchanges and electronic communication networks (ECNs) to execute transactions fast (20+ pre-risk checks taking less than 100 nanoseconds).

2011: Quantopian

The Quantopian was founded in 2011 by John Fawcett and Jean Bredeche. It was a two-pronged business model focused on algorithm developers and institutional investors. The focus was to create computerized trading systems and strategies for elements Quantopian could add to its offerings to institutional investors.

In this business model, successful developer-members were entitled to a royalty or commission from these investor-members, who earned profit from their strategies.

After several years, Quantopian was declared insolvent and was shut down by the authorities.

2012: From Tweets to Actionable Trading Signals

Dataminr, a New York-based start-up, launched a new service in September 2012. The service aimed to turn tweets and other social media communications into actionable trading signals. In this service, a lot of micro-trends can be identified, which helps clients foresee upcoming trends.

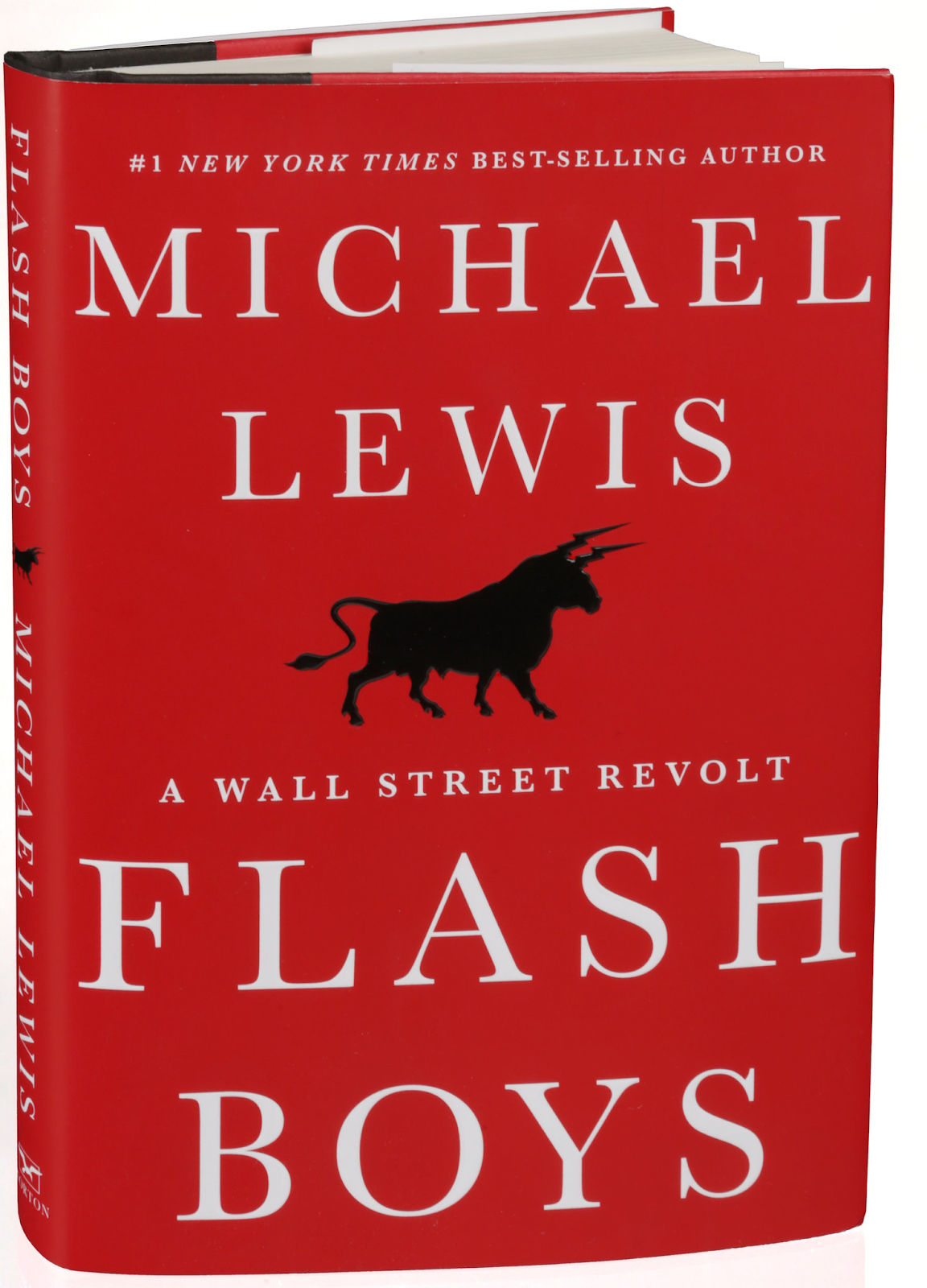

2014: Michael Lewis’s Flash Boys

In 2012, Michael Lewis published the best-selling book Flash Boys. The book narrates the lives of Wall Street traders and entrepreneurs who laid the foundation of electronic trading in the US.

Flash Boys gives light on the rat race among the tech companies to build faster computers to enhance the speed of information transfer between exchanges.

2015: CFTC Approved Proposed Rule on Automated Trading

The US Commodity Futures Trading Commission (CFTC) approved proposed rules for increased regulation of automated trading on US designated contract markets (DCMs). The purpose of this was to reduce potential risks from algorithmic trading activity.

2020: Trying Times for the COVID-19 Pandemic

In times of uncertainty like the COVID-19 pandemic, traders rely on algorithmic trading strategies for lower human errors and faster decision-making. Data showed that algo trading market share almost doubled to 20.75% in 2021 from 10.98% in 2020.

Conclusion

In the early years of algorithmic trading, it was designed for basic arbitrage, pairs trading, market-making strategies, and automation. Over the years, it has evolved to address the changing market conditions. In recent years, the development of algorithmic trading centers around machine learning and related technological advances.

want to learn how to algo trade so you can remove all emotions from trading and automate it 100%? click below to join the free discord and then join the bootcamp to get started today.